In insurance contracts for major development or municipal projects, there are generally a number of parties that have insurance coverage under a single insurance policy. For example, in The Burlington Insurance Company v NYC Transit Authority (No. 57), previewed here, a general contractor, Breaking Solutions, Inc. (BSI), was awarded a contract to complete some excavation work on a Brooklyn subway project. As a requirement of the contract, BSI was obligated to maintain a commercial general liability insurance policy and to name NYCTA, MTA New York City Transit (MTA), and New York City as additional insureds. As an additional insured under the policy, NYCTA, MTA, or the City could only obtain coverage for any losses they sustained as a result of “‘bodily injury,’ . . . caused, in whole or in part, by . . . acts or omissions” of BSI.

The issue here is whether the additional insureds would be entitled to the coverage if BSI, the named insured, was not negligent. During the project, a BSI excavating machine broke a buried electrical cable, which set off an explosion that injured a NYCTA employee. After the federal district court dismissed the employee’s claims against BSI with prejudice, Burlington settled the suit for $950,000.

Once Burlington settled the case, it disclaimed additional insured coverage for NYCTA and MTA because it was solely NYCTA’s responsibility to mark the buried electrical lines and turn off the power and its failure to do so was the sole cause of the explosion. Because BSI, the named insured, was not neglient and thus did not proximately cause the explosion, Burlington reasoned, the additional insureds were not entitled to coverage.

In the ensuing declaratory judgment action to confirm the disclaimer of coverage, Supreme Court held that NYCTA and MTA were not additional insureds entitled to coverage because none of BSI’s acts were negligent. In fact, because NYCTA failed to mark or deenergize the power lines before BSI began the work, there was no way for the BSI employee to know that a live wire had been buried beneath the spot where he was excavating. Supreme Court therefore held that NYCTA and MTA could not obtain coverage for the accident as additional insureds. The Appellate Division, First Department, however, reversed, and the Court of Appeals granted leave to appeal.

The Court of Appeals agreed with Supreme Court, holding that the policy only provided additional insured coverage if the injuries were proximately caused by the named insured, here BSI. No coverage is available where, as here, the injuries claimed arise solely from the negligence of the additional insured itself. The Court, therefore, rejected NYCTA’s and MTA’s interpretation of the insurance policy, which relied on “but for” causation to mean that additional insured coverage would have been available for any act of the named insured, regardless of whether the named insured was negligent.

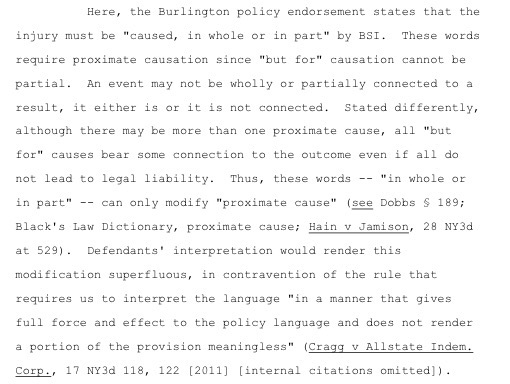

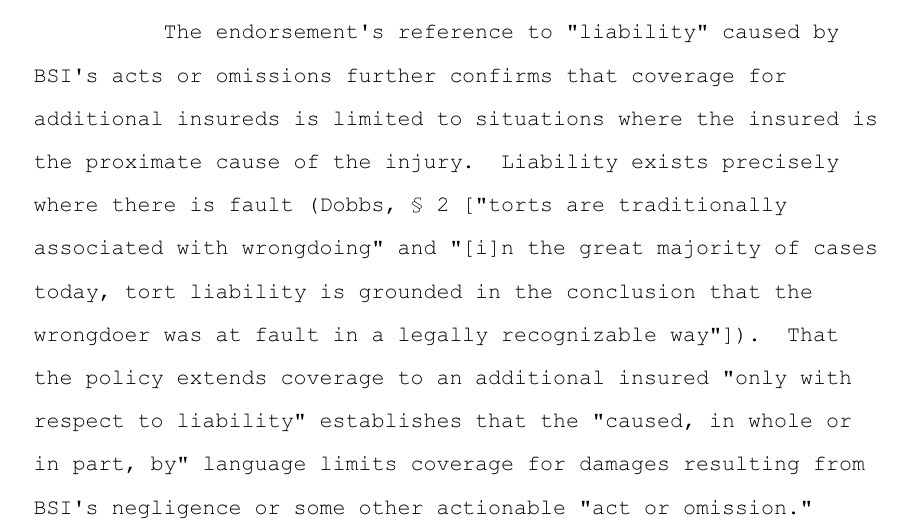

Further, the Court held:

After this decision, additional insureds should be aware that if the named insured has not been negligent or undertaken some other actionable conduct, insurance coverage likely will be unavailable.

The Court of Appeals’ opinion can be found here.